Investor Update – Navigating a Shifting Global Landscape

“When a clown moves into a palace, he doesn’t become a king. The palace instead becomes a circus.” ~ Turkish Proverb

The Situation

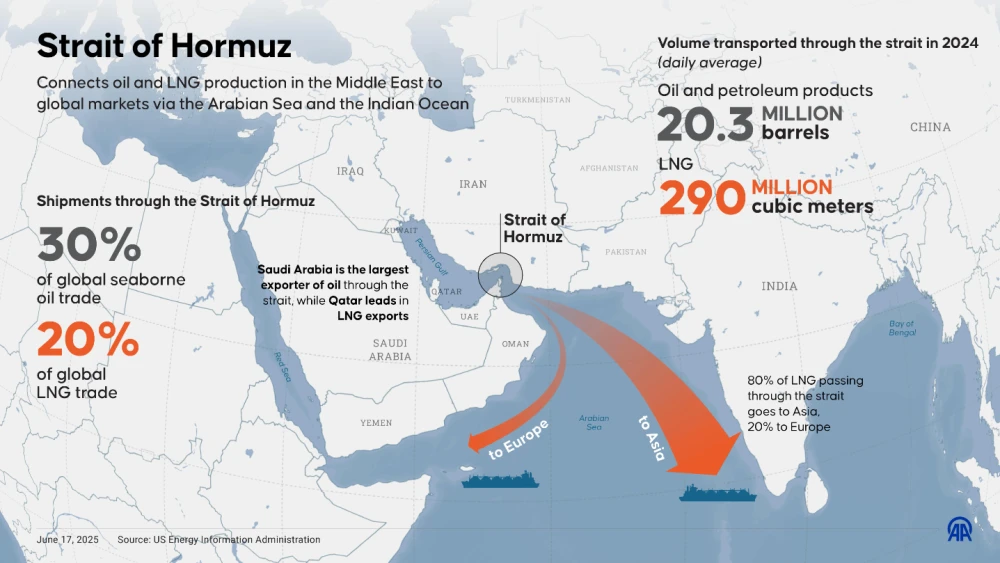

The Strait of Hormuz has quickly become one of the most important economic pressure points in the world today. At its core, this is the latest foray in a regional conflict, that has global consequences, driven by its direct impact on oil and natural gas flows.

This roughly 40km wide stretch of water has historically operated as an open international corridor, with structured lanes allowing hundreds of vessels to pass safely each day. Through it flows approximately a quarter of the world’s oil supply, a meaningful share of global natural gas, and a significant portion of the food and commodities required to sustain Gulf-region populations.

What makes this situation fragile is the nature of energy itself. Oil is consumed continuously and must be replenished daily. Even short disruptions can take months, and in some cases longer, to fully normalize once supply chains are interrupted.

A Different Kind of War

For decades, Iran has operated indirectly, projecting influence and waging war through groups such as Hezbollah, Hamas, and the Houthis, while avoiding direct conflict on its own soil.

Influenced by regional ally Israel, and betting that Iran was ripe for revolution, the United States took that war to Iranian soil, bombing military facilities and equipment.

Since the Iranian Revolution that ousted the US-friendly Monarchy, the Iranian Guard has been preparing, to some extent, for open conflict with the United States and their regional rival, Israel. Rather than engaging in a conventional military confrontation, Iran is applying pressure where the global system is most exposed. It is doing so at a fraction of the cost faced by traditional military powers.

This is showing up in two key ways:

- The use of low-cost drones and small vessels against significantly more expensive defense systems, and tankers

- Control access through the Strait of Hormuz

The second point is the more important one. Control of a critical trade corridor introduces leverage that extends well beyond the region. Countries are now faced with a choice. They can negotiate access, or they can source energy elsewhere, often at higher cost and with new geopolitical dependencies. The primary benefactors here are the world’s largest oil producers: the United States, and Russia.

This is no longer just a geopolitical conflict. It is an economic one, with strongly divisive geopolitical considerations, especially for countries like Europe or India that import much of its oil, and are engaged open conflict with at least one major alternative to middle-east oil.

Negotiation Realities: Iran thinks its ‘Winning’ the War

Disciplined, and dogmatic, they executed their plan to gain control over strait of Hormuz, providing both economic influence and negotiating leverage. There have been early signals of potential diplomatic pathways, including a multi-point framework reportedly advanced by the United States through Pakistan. These discussions appear to focus on:

- Cessation of nuclear ambitions

- Constraints on missile development

- Withdrawal of support for proxy groups

- Relinquishing control of the Strait

For its part, Israel had longer term ambitions, specifically geared to regime and leadership change. Its strikes have been largely focused on individuals and the apparatus

that it views as least likely to work towards meaningful change in the direction of Iran. Any negotiations that involve Israel will likely be predicated on a change in leadership within Iran.

The challenge is not defining the terms. The challenge is creating the conditions under which those terms would be accepted. At present, Iran appears to be operating from a position of strength, and views Israel and the United States as the aggressor. For these reasons, they have established a very different list of demands:

- End of hostilities and guarantees against future attacks by Israel & US

- Reparations and compensation for war damages for initiating the conflict

- Lifting of all sanctions against Iran

- Removal of US Military presence in the Region

- Permanent control of the Strait of Hormuz

A nation on its knees would not put forward these kinds of demands unless it felt it was in a position of power. For negotiations to move forward in a meaningful way, the United States would need to re-establish a position of clear strength. In practical terms, that likely requires a significant escalation, both financially and in terms of human cost.

That is a difficult path.

- It would require broad international alignment

- It would demand domestic political support

- It would introduce risks that extend well beyond the region

At this stage, it is not evident that the current U.S. administration, under Donald Trump, has the diplomatic leverage or allied support required to pursue that path. Specifically, NATO has hardened their stance on joining the war, while it has been reported on Israeli TV that their forces will not fight alongside the US in a ground war. Without a shift in the balance of power, negotiations are likely to remain limited.

While claiming military victory during a televised speech on April 1st, the President of the United States does not appear to have a clear exit strategy or peace framework. The justifications advanced by Donald Trump that Iran was on the path to acquire nuclear weapons and posed an imminent threat, are disconnected from the intelligence narrative. It’s combative stance towards its allies continues to undermine the prospect for international cooperation, and we have difficulty seeing a pathway to rapid resolution and resumption of oil flows.

Economic Implications

The economic impact of disruption in energy production follows a familiar pattern.

Oil prices move first. Inflation follows as higher input costs work their way through goods and services. Economic activity slows as both businesses and consumers become more cautious. We are already seeing early signs of this progression.

Higher inflation is also putting pressure on bond markets. Yields have adjusted upward, reflecting rising price expectations. This reduces the ability for central banks to cut interest rates or add liquidity to support growth. That has broader implications.

Liquidity has been a key driver of asset prices in recent years. With less room for central banks to ease policy, an important source of speculative capital is reduced. This can weigh on financial assets more broadly. Even gold, which is often viewed as a defensive asset, can face headwinds in this type of environment when inflation climbs at the same time as policy flexibility becomes constrained.

There is also a secondary effect that is less visible, but important. Disruptions to fertilizer and agricultural inputs can place additional pressure on global food prices over time.

Taken together, this creates a meaningful headwind for economic growth worldwide.

Portfolio Positioning

Our focus remains on preparation, not prediction. We entered the year with a modest overweight to energy (6%), recognizing the potential upside in a supply-constrained environment. That positioning has benefitted the portfolio and helped offset some of the damage so far, this year.

More broadly, our portfolios remain globally diversified and are not overly exposed to any single geopolitical outcome. This is intentional. It allows portfolios to absorb shocks rather than react to them.

At the same time, the tone in markets is beginning to shift:

- Institutional investors are becoming more cautious, which hedge funds reportedly at multi-year equity exposure lows

- Some of the strongest areas of the market, including AI-related investments, are facing more scrutiny (MSFT down 20%+ YTD)

- The risk of volatility and market pullbacks is increasing

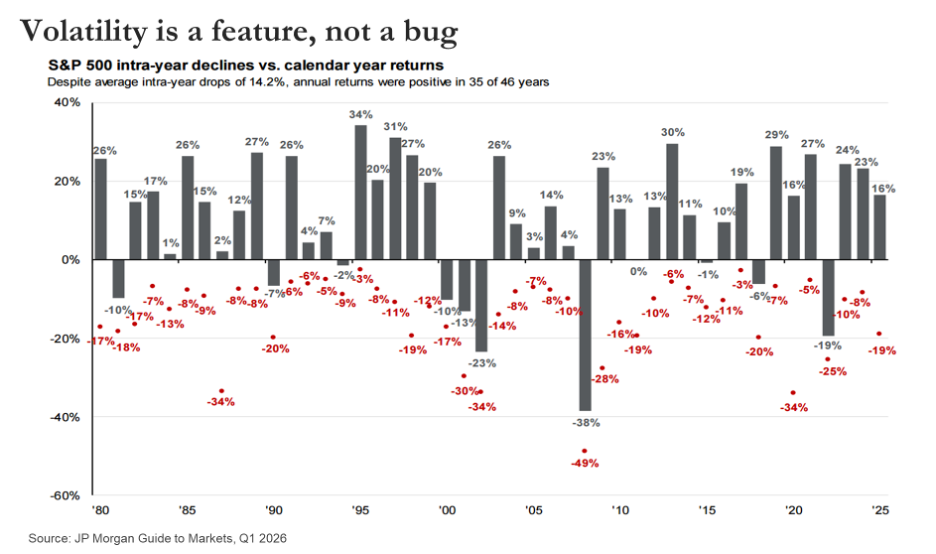

After several strong years, this is not unusual.

As evidenced by the graph, markets have been positive ~80% of years since 1980. Through these positive years, it is common for markets to suffer mid-year crashes and corrections, with these drops averaging -14% over this same time period. In other words, volatility is a feature of investing, not a bug.

Looking Ahead

As discussed, markets do not move in straight lines. They move between periods of optimism and pessimism, often pushing too far in both directions. A period of volatility would be a healthy development. It resets expectations and creates opportunity for disciplined investors.

With that in mind, we started the year defensively positioned in the Innova Tactical Pool. This was accomplished by:

- Building cash reserves (~10%) as at March 31st, 2026

- Preserving 6-8% of the portfolio in gold bullion

- Committing funds to stable, core infrastructure investments

- Incorporating hedging strategies where appropriate, given the close relationship between the Canadian dollar and the price of oil

This has led to a more measured start to the year – one grounded in a more defensive posture in the portfolio, despite our AI-fueled productivity optimism.

Closing Perspective

Periods like this can feel uncertain, particularly when regional conflict begins to influence global economic outcomes. Your portfolio and financial plan are built with uncertainty in mind, both allowing flexibility to react to changing world conditions.

Our role is to stay grounded, interpret what is happening, and position accordingly. We remain focused on protecting capital, managing risk, and identifying opportunities as they arise, with the objective of helping you reach your goals, and move forward with clarity and confidence.

As always, our team of advisors remains available to you to discuss your specific portfolio. On behalf of the team, Thank You for your continued trust.

This publication is for informational purposes only and shall not be construed to constitute any form of advice. The views expressed are those of the author alone. Opinions expressed are as of the date of this publication and are subject to change without notice and information has been compiled from sources believed to be reliable. This publication has been prepared for general circulation and without regard to the individual financial circumstances and objectives of persons who receive it. You should not act or rely on the information without seeking the advice of the appropriate professional.

- Hits: 2138