Bothersome Bonds - Explained

“The stock market is a device to transfer money from the impatient to the patient.”

— Warren Buffett

In times of “peak uncertainty”, it is often tempting to run for the hills and put all your money under the mattress or, in the investment world, move to cash or bonds. In this month’s newsletter we discuss why, despite adopting a defensive stance, we continue to hold more stocks than bonds in the portfolio.

As many of you know, the Innova Private Pool is founded on our tactical asset allocation strategy. Simply put, that means our strategy shifts between stocks, bonds, cash, gold, and other asset classes to reduce risk. Historically speaking, we have shifted primarily between stocks and bonds, the two largest, most liquid asset classes on the market; or put more simply, high-flying stocks when we felt greedy, the safety of bonds when we felt queasy.

More recently however, these two investments classes have begun to move more in synch, thus reducing their effectiveness as counterweights to one another. At the same time, mid-pandemic, the risks to bond investors have increased while falling interest rates have decreased their return potential. Furthermore, we feel the risk-to-reward considerations for bonds are not attractive at present and have thus decided to tactically reduce our exposure to bonds. To further explain why we feel the risk-to-reward considerations for bonds are not attractive at present, and as part of our continued commitment to increase your investment IQ, we present to you a short ‘Bond Investing 101’.

Bond Investing 101

In their simplest form, bonds, also known as fixed-income, are a loan to a company or government. Similar to a mortgage or any other loan, bonds have an interest rate and repayment terms, sometimes 10, 20, or 30+ years. When lending to a sufficiently credible lender, like a government or a large multi-national, the risk of them not making their payments, or ‘defaulting’, is quite low. As such, if you buy the bond when it is issued and hold it until maturity then your rate of return should be equal to the interest rate.

For example, let us say that you purchased a 10-year Government of Canada bond at 10% interest per year for $10,000 ten years ago. You essentially purchased a piece of paper on which the government has promised you to pay you your $10,000 principal in 10 years as well as $1,000 per year for all ten of those years (10% of $10,000). Nerd note: Some 50+ years ago, these promises to pay were issued with a physical ‘coupon’ that investors could rip off and bring to the bank in exchange for their annual payment. This is where the investment term ‘coupon’ for the payments from a bond are derived.

Since the Government of Canada has not (yet – UBI discussion anyone? 😊) defaulted on any loans, you would receive your 10% interest every year and then your full $10,000 in principal back in year 10. In other words, you made your full 10% per year with no loss on your original capital.

Where things get complicated however is when investors buy and sell bonds before they mature, or when they want to get the current value of their bonds, also known as the fair market value. In our example, let us look at year 5 of the 10-year bond’s life. The market value, or price you would get if you sold your bond in year 5, would be impacted by current interest rates more than any other factor.

Assuming no substantial changes in the default risk of the Government of Canada, the rate at which they issue new bonds, say 5%, will have a substantial impact on what people are willing to pay you for your $10,000 promise from the same bond-issuer. This influence is because a new bond, or promise from the same borrower, at 5% will receive $500 per year instead of your $1,000 per year, thus making your promise to pay more valuable.

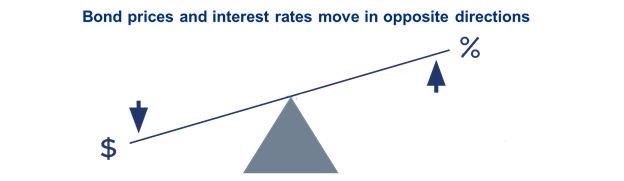

Since the risk of default has not changed, your bond will need to be priced to offer the same rate of return to investors as those offered by newly issued bonds. If rates on new bonds go DOWN, your older bond is paying more interest and so its market value will go UP. If rates have gone UP, and new investors receive more interest than you are offering, the price of your bond will go DOWN. This phenomenon is known as a negative correlation.

Fortunately for us, the bright minds of finance have derived a formula that provides a good approximation of what impact the rise or fall of interest rates might have on the market value of your investments. Known as duration, this one number gauges the percentage gain or loss on your portfolio due to changes in interest rates.

For example, a bond with a duration of 5 will lose 5% for every 1% increase in interest rates. A 1% drop in interest rates would mean a 5% gain to those same investors thanks to the negative correlation discussed earlier. All of which means, it is imperative that long-term bond investors pay close attention to their portfolio’s duration to understand the impact that interest rate changes might have.

To that end, we assembled the following table using Morningstar Advisor Workstation that shows the largest ‘Advisor’ version mutual funds to gauge the impact on the average Canadian.

As you can see, there are more than 100 billion dollars of Canadian investment capital currently held in these bond mutual funds, which have an average duration of 8.7. This figure means that a 1% increase in interest rates could result in a 8.7% drop in the value of low-risk bond investment.

It is also important to note that interest rates have dropped 1.5% so far this year, resulting in excellent returns for bond investors (Thank you Mr Poloz!). With the Bank of Canada’s target overnight rate at 0.25% and the Federal Reserve at 0.09%, so how much lower can rates go? The European and Japanese Central banks have experimented with negative interest rates, which we discussed in IMI#68 ‘An Upside Down World’.

Most experts agree that at some point rates will likely come back up. Although no interest rate increases are forecast in the near term(Sources 1&2) it’s questionable how many investors have braced themselves for a double-digit loss in their ‘low-risk’ investments.

Using the numbers above and a rate increase comparable to the decrease this year, a 1.5% jump in interest rates would result in a 13% loss to these investors. Tack on the 1.27% average MER and you end up with an almost 15% loss potential. Bear in mind that such an increase would only bring interest rates to where they were pre-CoViD, but still considerably below the 5.86%(Source 3) 30-year average.

If the loss potential on these investments is over 15%, what is the potential upside in our risk-to-reward equation? If interest rates in Canada drop to 0%, we could see a (0.25% * 8.7 =) +2% bump to tack onto the interest rates earned by the bonds for a total net return of 4-5%. Negative rates could see that return inch higher but would likely be accompanied by higher risks of default in corporate bonds.

For these reasons, we see the risk/return profile of bonds closer to -15%/+5% as it stands. With this in mind, we have actively been reducing our exposure to bonds. Long-term care facilities, apartment complexes, and agricultural land have all received additional allocations, while stocks remain a large part of the portfolio.

Although there is a still a place for bonds, specifically those that will ‘Zig’ when stocks ‘Zag’, we believe our current allocations to alternatives and stocks provide a better risk-to-reward relationship than bonds. Our overall stock portfolio is tilted to large multi-national companies whose business models should be able to survive and thrive during CoViD. In many cases, a reliable and growing dividend helps improve the cost of waiting for a vaccine.

Take Telus and Bell Canada as examples. They are offering 5% and 6% dividend yields at present and should be able to survive CoViD, no matter how long it lasts. This situation means that so long as the company can retain its customer base, we should receive a 5-6% per year return until a vaccine is propagated and the economy can return to normal. At that time, these stocks would likely benefit from the economic recovery that would ensue, providing further tailwinds to the investments.

For these reasons, when faced with a decision to allocate capital to stocks, bonds, OR alternatives, we have favoured stocks and alternatives over the presumed safety of bonds. That said, long-term government bonds in particular still provide a negative correlation to our current stock portfolio and so still feature in our top holdings. This is meant to act as a counterweight should the economy go through another significant downturn.

As always, we welcome the opportunity to discuss the specifics of your portfolio, so please do not hesitate to contact us.

Sources

[ihttps://www.bankofcanada.ca/2020/09/fad-press-release-2020-09-09/

[iihttps://www.federalreserve.gov/newsevents/pressreleases/monetary20200916a.htm

[iiihttps://tradingeconomics.com/canada/interest-rate#:~:text=Interest%20Rate%20in%20Canada%20averaged,percent%20in%20April%20of%202009.

Disclaimer:

Aligned Capital Partners Inc.(ACPI) is regulated by the Investment Industry Regulatory Organization of Canada (www.iiroc.ca) and a Member of the Canadian Investor Protection Fund (www.cipf.ca). Investment products are provided through ACPI and include, but are not limited to, mutual funds, stocks, and bonds. Please contact Jean-François Démoré or Cliff Richardson, or visit https://invest.innovawealth.ca for additional information about the Innova Tactical Asset Fund. All non-securities related business conducted by Innova Wealth Partners is not as agent of ACPI. Non-securities related business includes, without limitation, fee-based financial planning services; estate and tax planning; tax return preparation services; advising in or selling any type of insurance product; any type of mortgage service. Accordingly, ACPI is not providing and does not supervise any of the above noted activities and you should not rely on ACPI for any review of any non-securities services provided by Jean-François Démoré or Cliff Richardson.

Information has been compiled from sources believed to be reliable. All opinions expressed are as of the date of this publication and are subject to change without notice. Content is prepared for general circulation and has been prepared without regard to the individual financial circumstances and objectives of persons who receive it. The information contained does not constitute an offer or solicitation to buy or sell any investment fund, security or other product or service. Past performance is not indicative of future performance, future returns are not guaranteed, and a loss of principal may occur. Content may not be reproduced or copied by any means without the prior consent of the author and ACPI. For current performance information, please contact Innova Wealth Management of Aligned Capital Partners Inc. Important information about the Fund is contained in the offering memorandum which should be read carefully before investing.

- Hits: 8452