CoViD & Corrections

“The time to buy is when there is blood in the street. Even your own.” - John D. Rockefeller

Understandably, the past few months have been a time of great uncertainty and anxiety for all investors. Retirees and even those with decades of investing ahead of them share mutual concerns and question whether it’s time to run from the markets and move to cash, or to double down. Most observers agree that things will likely get worse before they get better.

We have received an equal number of emails asking whether it is the time to move to cash or to buy low as we have questions about how we see this all playing out and the impact on our investment portfolio.

To that end, this issue of Innova Market Insights (IMI) is a breakdown of what we expect to materialize as our ‘most likely’ scenario for CoViD-19 and how it is shaping our investment policy. The following was greatly influenced by this excellent piece (at least, in our view!) by epidemiologist Dr. Raywat Deonandan.

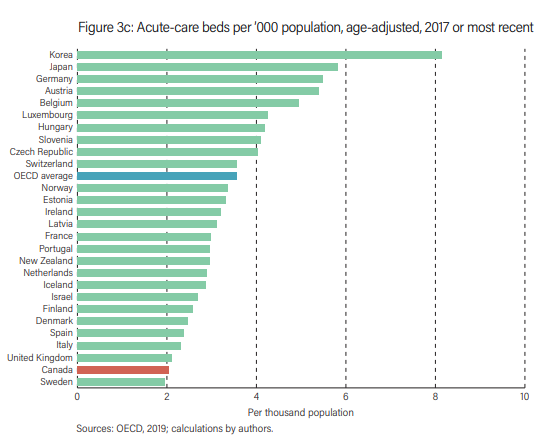

According to a few sources ([i],[ii]), Canada has somewhere between 70,000-75,000 acute care hospital beds across the country.

Even a conservative estimate wherein 50% of the population gets infected and 1-2% of those individuals require emergency care, we are still short a few hundred thousand beds, which doesn’t account for any other medical needs for beds… Obviously, this is a situation that needs to be dealt with, but so far neither Federal nor Provincial governments have made any headway on increasing the number of beds. They also haven’t created temporary locations for testing, medically assisted isolation, or treatment centers, yet south of the border, work has begun : New York adds 2000 beds in a single location.

Given the limited capacity to handle a large influx of patients, the national policy is to try and ‘flatten the curve’ or defer the inevitable. The only thing they have managed to accomplish so far is to throw money at the people who are staying home, rather than creating the infrastructure to handle a potential crisis.

According to Dr. Deonandan, the two most likely ways in which this pandemic will fully run its course are:

- Herd Immunity

At some point, enough people will have been infected by the disease and develop natural immunity, or a vaccine will come along and save the day. Realistically, we are at least 12 months away from a commercially viable vaccine coming along while the number of people required to reach natural herd immunity would leave millions of dead in its wake.

- Extreme Isolation (30+ days)

The nuclear option. Take the existing quarantine and push it to the limit in which even grocery stores are closed to eliminate the possibility of the virus spreading until it ‘dies out’.

Both options are far from appealing from a social or economic viewpoint. The more likely outcome is that we enter a ‘new normal’ in which rolling isolations become commonplace. Basically, we go in and out of these ‘non-essential workplace quarantines’ whenever we have flare-ups of CoViD-19 to contain and slow the spread so that our health system can manage it, until the herd immunity is reached by means of vaccine or natural immunity.

In the meantime, what happens to the economy? Governments have been asking themselves this very question and investigating support measures in these unprecedented times. Employment insurance, sick leave top ups, financial support to families, hydro rate cuts, and various experimental policies are being tried. What will or will not work is anyone’s guess.

Equally difficult to predict is what will happen to the stock market.

The anatomy of a correction

In our research, we have observed that stock market corrections typically occur in three stages over 4-6 months on average.

|

1. The Shock

2. The Stutter

3. The Shudder |

|

In the first stage, The Shock, investors react with incredulity. Not fully understanding the ramifications of the event, markets swing wildly with large negative days quickly followed by rapid rebounds. Fear and greed, the two overlying emotions that drive market sentiment, are in a constant back-and-forth. The extreme volatility usually lasts a few weeks and then gives way when capitulation occurs and investors with weak stomachs, or those unprepared for unforgiving markets, throw in the towel and accept massive losses. We saw early signs of this capitulation the week of March 16th to 20th when stock and bond exchange traded funds, the preferred vehicle of the inexperienced investor, underwent a total collapse in valuations under unbearable selling pressure. DIY investors were pulling out at any price!

This is commonly followed by a Stock Market Stutter in which stock markets start to recover quickly, only to lose momentum. Following a few good days, like the one we saw on Tuesday, March 24th during which the TSX rallied 12%, these same investors who were willing to sell ‘at any price’ a few weeks past, are now suddenly looking to ‘get back in’ at any price! Not wanting to miss out on any more of the ‘recovery’ they push markets beyond fair market value in the face of the new economic reality.

While the two first stages were ongoing, it is easy to forget that most companies only issue their financial statements quarterly, and so all the buying and selling was merely speculation. What is happening to companies versus what the actual financial statements will show is still unknown. As the reports get released and the real economic damage becomes quantifiable, the final stage of the correction, The Shudder, takes hold. Usually the longest lasting and the most difficult on the investor psyche, this phase can last 6-9 months before a recovery starts to take place. This stage is also when we find out what companies have been swimming without a bathing suit, as when the economic tide recedes, companies without strong financials (balance sheets) risk getting swept away. During these times, diligent stock pickers can thrive.

From that point, recovery ensues. On average, bear markets have taken an average of 14 months[i] to recover their losses. For a great summary on these soul crushing moments in history, give this a read.

Where are we now, and what is our strategy?

As alluded to earlier, we believe we are starting to see the signs of market capitulation on behalf of participants. Simply put, we have reached the breaking point for a lot of investors. What is unique about this particular correction is that the news, potential damage, and in turn, fear, will only get worse as the virus continues to spread. For this reason, calling the bottom will be incredibly difficult.

Our tactical asset allocation strategy, on which JF authored his Master’s thesis, looks to profit from these very moments in history. This strategy is similar to what some call the neutral zone trap.

“We are borrowing the name from hockey, in which ‘the trap’ is a tactic in which three to four players position themselves in the neutral zone with one or two of them selectively entering the offensive zone looking to take advantage of an error by the other team. Generally, the trap is a defensive strategy that teams use to protect a lead. In regards to managing a portfolio, our version of the trap aims to protecting against large market declines by remaining well diversified. This doesn’t mean you shouldn’t go on offence, but rather pick your spots by avoiding excessive risks, such as timing the bottom”

PELLETIER, Martin: Why buy and hold may not be the best strategy for the coronavirus selloff

As detailed in our last few IMI updates, we had taken a fair bit of stocks off the table (Tactical Asset Allocation) before this correction started and so, with the markets having been down 30%+, it is our opinion that we have a ‘lead’ that we want to protect. At the same time, we want to be opportunistic and be able to profit when the markets eventually recover.

For that reason, we have been selectively buying stocks on particularly nasty days, and occasionally offloading stocks during up markets that we feel have gotten ahead of themselves. Since our last update on March 12th, we have been net buyers. The following table illustrates our asset allocation inside of the Innova Tactical Asset Allocation Private Pool since the market peak.

As you can see, we have been extremely active in our asset allocation and shifted positions in response to the rapidly changing markets and investor reactions. Currently, we have invested about 1/3 of the portfolio in stocks, which will increase our ability to participate more in market rallies and the coming drops.

For these reasons, we remain defensive with our core positions, holding quality companies whose business models and financial strength should allow them to survive the scenarios outlined above. Sectors like telecommunications, e-commerce, consumer defensive and utilities contain the types of names that we are adding to the portfolio, as well as a few undervalued positions, as market opportunities present themselves.

Like you, we are concerned with what will come of the CoViD-19 pandemic and its economic fallout, specifically as it pertains to ‘main street’ small businesses. That said, we will continue to monitor the markets for opportunities to protect your assets and provide long-term profits for investors.

Thank you for your continued trust,

J-F, Cliff & the Innova Team

[i] https://www.fidelity.com/viewpoints/market-and-economic-insights/bear-markets-the-business-cycle-explained

[i] https://www.ncbi.nlm.nih.gov/pmc/articles/PMC3999549/

[ii] https://www.fraserinstitute.org/sites/default/files/comparing-health-care-countries-2019.pdf

Disclaimer:

Aligned Capital Partners Inc.(ACPI) is regulated by the Investment Industry Regulatory Organization of Canada (www.iiroc.ca) and a Member of the Canadian Investor Protection Fund (www.cipf.ca). Investment products are provided through ACPI and include, but are not limited to, mutual funds, stocks, and bonds. Please contact Jean-François Démoré or Cliff Richardson, or visit https://invest.innovawealth.ca for additional information about the Innova Tactical Asset Fund. All non-securities related business conducted by Innova Wealth Partners is not as agent of ACPI. Non-securities related business includes, without limitation, fee-based financial planning services; estate and tax planning; tax return preparation services; advising in or selling any type of insurance product; any type of mortgage service. Accordingly, ACPI is not providing and does not supervise any of the above noted activities and you should not rely on ACPI for any review of any non-securities services provided by Jean-François Démoré or Cliff Richardson.

Information has been compiled from sources believed to be reliable. All opinions expressed are as of the date of this publication and are subject to change without notice. Content is prepared for general circulation and has been prepared without regard to the individual financial circumstances and objectives of persons who receive it. The information contained does not constitute an offer or solicitation to buy or sell any investment fund, security or other product or service. Past performance is not indicative of future performance, future returns are not guaranteed, and a loss of principal may occur. Content may not be reproduced or copied by any means without the prior consent of the author and ACPI. For current performance information, please contact Innova Wealth Management of Aligned Capital Partners Inc. Important information about the Fund is contained in the offering memorandum which should be read carefully before investing.

- Hits: 7798